Table of Content

While we adhere to stricteditorial integrity, this post may contain references to products from our partners. Sandra is qualified as a financial advisor with business accreditation and has an eye for detail. She got her start in the banking industry working with small businesses and startups – and she can tell a good deal from a shiny gimmick.

The buyer does not need to generate a new loan to purchase the house. This becomes a popular feature when interest rates rise, because the older existing loans will usually have lower rates. A wrap around mortgage is not the same as assuming an existing mortgage that has already been created.

How to Assume a Mortgage

An assumable loan can make the home more marketable if interest rates have risen in the years since the mortgage was originated. Imagine a situation in which someone gets an assumable mortgage with a 4.75% interest rate and then sells the house five years later when interest rates are around 7%. That 4.75% rate, impossible to get otherwise, could tempt buyers to choose that house over another. An assumable mortgage allows a home buyer to not just move into the seller's former house, but to step into the seller's loan, too. This means that the remaining balance, repayment schedule and rate will be taken over by the new owner. There are certain situations where you may want to assume a mortgage.

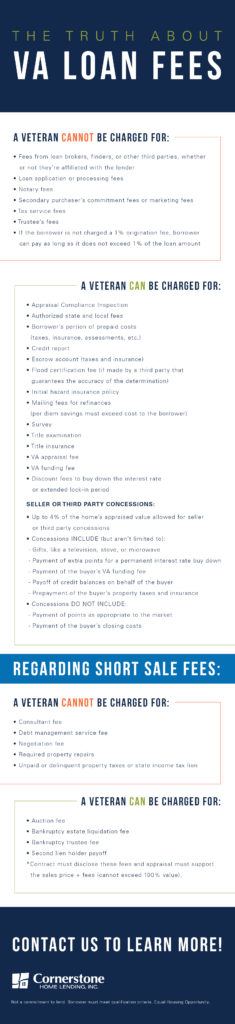

When determining the pros and cons of taking over a mortgage, you’ll want to consider any additional costs, paperwork and time frames needed to process the loan. While it may make sense to avoid higher interest rates through the seller's lender, it may be beneficial to shop around before committing to anything officially. Here’s what you need to know to decide if taking on an assumable loan is the right choice. The ability to assume a VA Loan is a great feature of the VA Home Loan Benefit. It allows a Veteran or active duty homeowner to sell their home to another willing and able buyer and have the new buyer assume the sellers existing VA home loan.

Assumable Mortgage Pros And Cons

As a result, if a future default and the subsequent claim are paid, the buyer is a creditworthy purchaser who agrees to pay their share of the payment obligation. In this case, their entitlement is substituted, and your VA entitlement is restored. If a civilian or non-eligible service member assumes your loan, your VA entitlement cant be restored until the loan has been fully repaid. In this situation, youll need to consider other mortgage options to buy a new home. If you decide to purchase a new home, you can use your portion of the proceeds from the sale to pay off any money you owe your ex-spouse for their interest in community property you shared.

You might be able to purchase your dream home if you assume a VA mortgage and save some money at the same time. Submitting evidence of on-time mortgage payments for the previous twelve months. Before you apply for any mortgage, brush up on ways to improve your credit score to put your best foot forward in your application. There is also an even easier way to find assumable VA loans.

How Much Can I Mortgage My House For

There are several websites, like TakeList, where you can find listings for assumable VA mortgages. These sites provide you with all the details, including the balance amount, interest rate, and seller’s exchange expectations. However, you must also remember that substituting the entitlement is only possible if the new owner is an eligible Veteran or a service member.

VA loans are approved for veterans, current military personnel, and spouses who qualify for the benefits of serving their country while in the military. As part of the VA loan assumptions, the assuming borrower must be financially qualified for the mortgage, regardless of whether the borrower is a veteran or not. There are parties who participate in unauthorized assumable mortgages, without involving the lender. The possibilities all depend upon what is outlined in the mortgage contract, which is a legal document.

However, exceptions to this rule exist to protect people going through significant life events. After a death or divorce, for instance, mortgage assumption can help families transfer mortgaged assets even without the approval of the lender. However, if you have a conventional adjustable-rate mortgage and meet certain financial qualifications, it’s possible that your mortgage is eligible for assumption. Prepare for the costs – You’ll need to make a down payment, but the amount depends on how much equity the seller has.

By communicating with us by phone, you consent to calls being recorded and monitored. But, like all similar questions, the answer will depend on your circumstances and needs. If you get the chance to assume a mortgage at an appreciably lower rate than you can get elsewhere, you should definitely run the numbers. If you want to assume any of these loans, you have to be eligible. The good news is, with a novation, the original borrower walks away free and clear.

Each spouse would need to be on the loan, meaning each person would be financially obligated and would need to meet requirements for credit score and other guidelines. A mortgage that has been assumed by a third party does not mean that the seller is relieved of the debt payment. The seller may be held liable for any defaults which, in turn, could affect their credit rating. Usually, a buyer will take out a second mortgage on the existing mortgage balance if the seller’s home equity is high. The buyer may have to take out the second loan with a different lender from the seller’s lender, which could pose a problem if both lenders do not cooperate with each other.

… If a lender accelerates a loan, the borrower has to immediately pay the entire balance of the loan, not just the current due payment. Clearly, an assumable mortgage makes little sense when mortgage rates are falling. Theres no advantage in taking over an existing loan when its rate is higher than one you can get by making a new application. Its important to ensure that the lender has signed off on the assumption, because they determine who is ultimately responsible for payment on the loan. Until the seller is released from liability by the lender, they are responsible for the debt, and nonpayment by the would-be assumer of the loan could negatively impact their credit score.

You do not need to visit a regional office for approval if your lender has automatic authority. However, if this is not the case, you would have to seek the lender’s permission and the VA to assume a mortgage. Here are the pros and cons that come with assuming a VA mortgage. Additionally, transferring the mortgage liability to another party can be beneficial for a person moving and leaving their home behind. You can also opt to assume a VA loan in case of a divorce, and you wish to keep the home’s remaining equity. In this article, we’ll discuss everything you need to know about the VA loan assumption.

Or the buyer will need a separate mortgage to secure the additional funds. There could be a cost-saving advantage if current interest rates are higher than the interest rate on the assumable loan. In a period of rising interest rates, the cost of borrowing also increases. When this happens, borrowers will face high interest rates on any loans approved.

If the unique mortgage stability was $200,000 and the customer assumes the loan at a stability of $160,000, the customer should give you $40,000 in money to succeed in the unique stability. The customer might need to take out a second loan to give you that determine, which can or might not negate the advantage of a decrease rate of interest. The one destructive of an FHA loan is its price, says Pascarella. But when a stable credit score rating and down fee are a stretch for you, an FHA loan could be your solely choice. For lenders without automatic authority, the loan must be sent to the appropriate VA Regional Loan Center for approval. An even easier method of finding assumable VA mortgages is to get in touch with a real estate agent who can access MLS listings to help you find your next home.

When you assume a seller’s mortgage, you’re assuming all of their monthly payments and liability. If a serviceman or woman is required to move quickly on orders, for example, they may not have enough time to sell their house, restore their entitlement and purchase a new home fast enough. If another eligible veteran is able to assume their loan, then their entitlement is restored and they can use their VA benefit again in the future. Keep in mind, both the VA and the current lender have to approve the assumption.

No comments:

Post a Comment